We’ve created this guide, including the FAQs below, to help you understand the health coverage options and financial assistance available to you and your family in New York. The options found in New York’s Marketplace may be a good choice for many consumers, and we will guide you through the options below.

New York residents use a fully state-run health insurance Marketplace known as NY State of Health , where a dozen private insurers offer health plans . 1

The Marketplace also provides residents access to apply for the state’s Basic Health Program known as the Essential Plan (BHP), 2 which offers premium-free coverage to residents whose income is too high to qualify for Medicaid or Child Health Plus, but not more than 250% of the federal poverty level. This income limit was previously 200% of FPL, but increased to 250% of FPL as of April 2024, making premium-free Essential Plan coverage newly available to 100,000 additional New Yorkers. 3

New York is also seeking federal approval to use 1332 waiver pass-through funding to provide additional cost-sharing reductions for some Marketplace enrollees starting in 2025. 4

NY State of Health also offers a small business portal where employers with up to 100 employees can compare group health plans. In most states, “small group” means up to 50 employees, but New York is one of four states where small group plans are available to groups of up to 100 employees. 5

Hoping to improve your smile? Dental insurance may be a smart addition to your health coverage. Our guide explores dental coverage options in New York.

Learn about New York's Medicaid expansion, the state’s Medicaid enrollment and Medicaid eligibility.

Use our guide to learn about Medicare, Medicare Advantage, and Medigap coverage available in New York as well as the state’s Medicare supplement (Medigap) regulations.

Short-term health plans provide temporary health insurance for consumers who may find themselves without comprehensive coverage. Learn more about short-term plan availability in New York.

To purchase health coverage through the New York Health Insurance Marketplace, you must: 6

Eligibility for financial assistance (premium subsidies and cost-sharing reductions) depends on your household income. In addition, to qualify for financial assistance with your New York Marketplace plan you must:

In New York, the open enrollment period has both a start and end date that differ from the schedule used in most other states (as noted below, the start date is expected to change for 2025 coverage, due to new federal rules). Open enrollment in New York starts November 16, and normally continues through January 31. 10

For 2024 coverage, however, New York State of Health kept enrollment open through May 31, 2024, due to the “unwinding” of the pandemic-era continuous coverage rule for Medicaid. So enrollment in 2024 qualified health plans in New York continued through May 2024, without the need for a qualifying life event. 11

For 2025 and future years, the federal government has finalized a rule change that requires all state-run exchanges to begin open enrollment on November 1 (or earlier, if a state was already using an earlier date), and end it no sooner than January 15 (or earlier if a state was already using an earlier date). 12 So the expectation is that New York’s open enrollment period will switch to having a November 1 start date, beginning with the enrollment period in the fall of 2024.

Enrollment in Medicaid, Child Health Plus, and the Essential Plan continues year-round for eligible people.

For qualified health plans (ie, not Medicaid, CHP, or the Essential Plan), enrollment outside of the annual open enrollment window is only possible if you qualify for a special enrollment period, which is typically triggered by a specific qualifying life event.

New York is one of several states where pregnancy counts as a qualifying event. In most states, it’s the birth that triggers a special enrollment period, but New York allows the expectant mother to sign up for health insurance due to the pregnancy. 13

If you have questions about open enrollment, you can learn more in our comprehensive guide to open enrollment . We also have a comprehensive guide to special enrollment periods .

To enroll in an ACA Marketplace plan in New York, you can:

You can contact NY State of Health by phone at 1-855-355-5777 (TTY: 1-800-662-1220)

New York residents use NY State of Health to enroll in health coverage and obtain income-based subsidies.

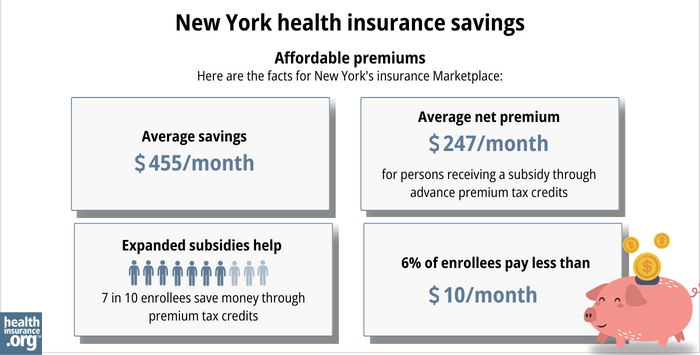

In the New York exchange, about 70% of enrollees were receiving premium subsidies as of early 2024 with an average subsidy of $455/month. After the subsidies were applied, enrollees’ net premiums averaged $247/month for those eligible for subsidies. 15

In addition to the private qualified health plans available through the state exchange, almost 1.2 million people were enrolled in Basic Health Program coverage through New York’s Essential Plan as of January 2024, and that had grown to almost 1.4 million by May 2024 (as described below, eligibility was expanded in April 2024, leading to increased enrollment). 16 Essential Plan enrollment is completed via NY State of Health, just like qualified health plan enrollment. But BHP coverage in New York dwarfs qualified health plan enrollment. 17

The Essential Plan has zero premiums and low cost-sharing. It was previously available to adults with household incomes up to 200% of the poverty level. But the state obtained federal permission to extend the eligibility limit to 250% of FPL, starting in April 2024. 3 For a single adult in 2024, this allows access to the Essential Plan with a household income of up to $37,650. 18

(New York had previously paused the proposal to extend Essential Plan eligibility in the fall of 2023, 19 but subsequently asked the federal government to continue with the review and approval process, 20 including an addition to ensure that DACA recipients can enroll in the Essential Plan — which was granted as part of the waiver approval. 3 )

subsidy through advance premium tax credits. Expanded subsidy help - 7 in 10 enrollees save money though premium tax credits. 6% of enrollees pay less than $10/month. " width="700" height="355" />

subsidy through advance premium tax credits. Expanded subsidy help - 7 in 10 enrollees save money though premium tax credits. 6% of enrollees pay less than $10/month. " width="700" height="355" />

In addition to the ACA’s premium tax credits (subsidies), people with household incomes up to 250% of the federal poverty level also qualify for cost-sharing reductions(CSR) that reduce the out-of-pocket costs on Silver plans.

Because Essential Plan coverage now extends to 250% of the poverty level in New York, cost-sharing reductions are no longer available for new enrollees in the Marketplace, as they’re eligible for the Essential Plan instead.

But 22% of the people who enrolled during open enrollment for 2024 — when Essential Plan eligibility still ended at 200% of FPL — were eligible for CSR benefits. 15

In 2024, New York is seeking federal permission to modify the 1332 waiver that allowed for the extension of the Essential Plan. The state hopes to use pass-through funding to provide cost-sharing reductions to Marketplace enrollees with income up to 400% of the federal poverty level, as well as cost-sharing reductions for diabetes treatment and for pregnant or postpartum people. If approved, these benefits would be available for the 2025 plan year. 4

A note about standardization of qualified health plans in New York: Insurers that offer plans through NY State of Health must offer one standard plan design in each metal level in every county where the insurer offers plans (here are the 2024 standardized plan details). Carriers can also offer up to two non-standard plan designs at each metal level. 22

Since 2021, New York has required state-regulated (non-self-insured) health plans, including Marketplace plans, to cap out-of-pocket costs for insulin at no more than $100 per month. 23 Legislation passed in the Senate in 2023 to lower that cap to $30, but did not advance in the Assembly. 24 In 2024, the Senate passed legislation to eliminate cost-sharing for insulin, but it had not been taken up by the Assembly as of mid-2024. 25

T welve insurers offer 2024 qualified health plans on the New York exchange. There are also a dozen insurers that offer Essential Plan coverage for 2024 (the two lists are nearly the same, but there are some insurers that only offer one or the other). 1

All 12 insurers have filed rates and plans for 2025. 26

For 2025, the insurers that offer individual/family health plans in New York (including two that only offer plans outside the exchange) have proposed an overall weighted average rate increase of 16.6%. 27 This is a significant increase, but the rates are under review by the NY Department of Financial Services, which has historically approved rate increases that are quite a bit smaller than the insurers initially proposed.

The NY State of Health insurers have proposed the following average rate increases (before subsidies are applied) for 2025 individual/family health plans: 26

Source: New York State Department of Financial Services 26

It’s important to understand that net rate changes for people who receive premium subsidies can be quite different from the overall rate changes for that person’s plan, since it also depends on how the benchmark plan (second-lowest-cost silver plan) premium changes.

For perspective, here’s a summary of how average full-price (pre-subsidy) premiums for qualified health plans in New York’s individual/family market have changed over the years:

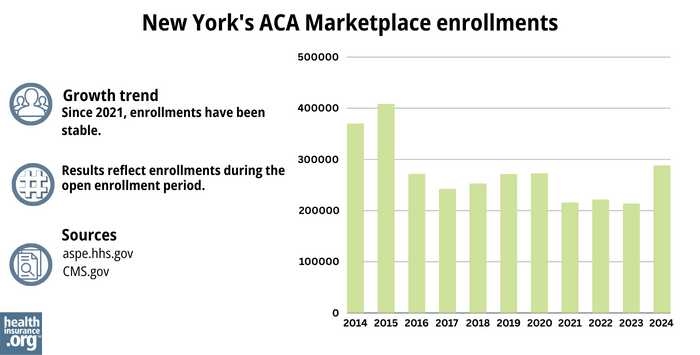

CMS reported that 288,681 people enrolled in private qualified health plans through NY State of Health during the open enrollment period for 2024 coverage (this total does not include Essential Plan enrollments).[ efn_note]” Health Insurance Marketplaces 2024 Open Enrollment Period Report ” CMS.gov. March 22, 2024[/efn_note]

Open enrollment continued through May 31, 2024 in New York (it normally ends January 31, but was extended due to the “unwinding” of the Medicaid continuous coverage rule). 11

But by early May 2024, enrollment in QHPs through NY State of Health had dropped to 233,151. 38 This was due to the expansion of Essential Plan eligibility starting in April, when people with household income between 200% and 250% of FPL became eligible for the Essential Plan and were able to transition from QHPs to the Essential Plan.

The chart below shows enrollment in NY State of Health QHPs over time. Enrollment in QHPs dropped in 2016 when the Essential Plan debuted, because many people previously eligible for subsidized QHPs transitioned to the Essential Plan starting in 2016. The same thing is happening in 2024 with the expansion of the Essential Plan.

But earlier in 2024, QHP enrollment was higher than it had been in several years. The enrollment growth in 2024 was likely driven by a combination of the continued subsidy enhancements under the American Rescue Plan, as well as the Medicaid unwinding process that began in the spring of 2023. By March 2024, more than 1.5 million people in New York had been disenrolled from Medicaid. 39

Some of them had transitioned to QHPs in the Marketplace, helping to drive 2024 enrollment. CMS reported that by February 2024, nearly 75,000 New York residents had transitioned from Medicaid to a qualified health plan in the Marketplace, and more than 317,000 had transitioned to Essential Plan coverage. 40

The chart below shows QHP enrollment by year in New York. But it’s important to note that New York’s Basic Health Program (BHP) covers far more people than the QHPs in the state, with nearly 1.4 million people enrolled in New York’s BHP as of May 2024. 16

Source: 2014, 41 2015, 42 2016, 43 2017, 44 2018, 45 2019, 46 2020, 47 2021, 48 2022, 49 2023, 50 2024 51

State Exchange Profile: New York

The Henry J. Kaiser Family Foundation overview of New York’s progress toward creating a state health insurance exchange.

Louise Norris is an individual health insurance broker who has been writing about health insurance and health reform since 2006. She has written dozens of opinions and educational pieces about the Affordable Care Act for healthinsurance.org.